Mortgage Affordability

Posted by JSCFinancial on Tuesday 20th of September 2022.

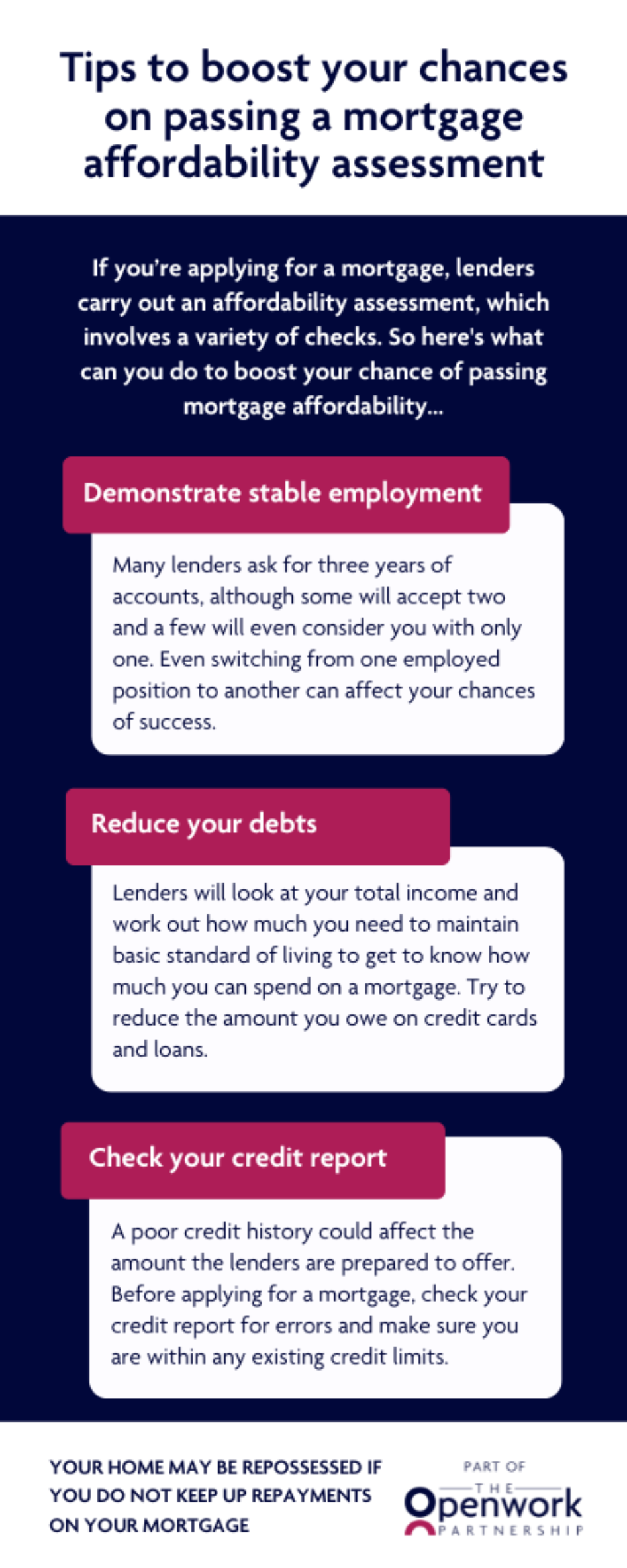

Improving your chances of passing a mortgage affordability assessment

The covid pandemic put things into perspective for Deborah. Before hand-sanitizer and facemasks became the norm, she and her boyfriend were living in a pokey flat while they saved up to buy a place of their own. As the pandemic took hold, they were both furloughed and - for the first time in years - had lots of free time together. This ultimately spelt the end for their relationship. Deborah moved back in with her parents and, to distract herself from this depressing development, got out her old sewing machine and starting upcycling second-hand clothes. Intrigued to know if there might be a market for her designs, she set up a simple online shop. Her clothes were a huge hit and, before she knew it, Deborah had a viable business on her hands.

Since going back into the office, Deborah’s realised how unfulfilling she finds her nine-to-five and is seriously considering quitting to focus on her upcycling business. However, she’s also determined to buy a place of her own within the next six months and doesn’t want anything to jeopardise her chances of passing a mortgage affordability assessment.

So how do lenders decide whether to offer you a mortgage?

If you’re applying for a new mortgage, remortgaging or increasing your current mortgage, lenders are required to carry out an affordability assessment. This involves a variety of checks designed to make sure you can afford to repay what you borrow. According to the Independent, some two thirds of first-time buyers are rejected for a mortgage at their initial attempt, so clearly these checks aren’t just for show. So what can Deborah do to boost her chances passing an affordability assessment

1.Demonstrate stable employment

Lenders are reluctant to offer mortgage deals to people who have recently become self-employed. Many ask for three years of accounts, although some will accept two and a few will even consider you with only one. Even simply switching from one employed position to another can affect your chances of success. Most lenders like to see that you’ve been with an employer for at least three to six months before they’ll consider you. With this in mind, it would make sense for Deborah to secure a mortgage first and then think about what she wants to do career-wise

2.Reduce her debts

Lenders will look at Deborah’s total income and then work out how much she needs to maintain a basic standard of living. This will give them an idea of how much she can afford to spend on a mortgage. Reducing the amount she owes on things like credit cards and loans will increase the amount she has available and boost her chances of passing an affordability assessment

3.Check her credit report

Before offering you a mortgage, lenders check your credit report. A poor credit history could affect the amount they’re prepared to offer or cause them to turn you away altogether. However, there are simple ways to improve your credit rating. Before applying for a mortgage, Deborah should check her credit report for errors, make sure she’s registered to vote at her mum and dad’s address, avoid applying for new credit in the six months leading up to her application and make sure she’s well within any existing credit limits

4.Get professional advice

A mortgage adviser will be able to assess Deborah’s circumstances and point her in the direction of the right lenders.

If you want advice on passing a mortgage affordability assessment, we’ll be happy to help.

Key takeaways:

- Lenders like to see that you have a stable income so it’s best to avoid changing your work situation in the time leading up to a mortgage application.

- Reducing the amount you owe on credit cards and loans can help improve your chances of securing a good mortgage deal.

- Lenders will check your credit report before offering you a deal so make sure yours is up to scratch before submitting a mortgage application.

- Professional advice could boost your chances of passing an affordability assessment.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE.

Please note: by clicking this link you will be moving to a new website. We give no endorsement and accept no responsibility for the accuracy or content of any sites linked to from this site.