Investing for your children's future

Posted by JSCFinancial on Wednesday 29th of June 2022.

As parents to four children ranging in age from three to 12 years old, Rachel and Samantha were horrified to hear on the news that a quarter of 20-to-34 year olds still live at home with their parents. As much as they love their kids, the idea they might still be a permanent fixture around the house into their 30s terrifies them.

Are Rachel and Samantha right to be concerned?

The short answer to this is yes! Research by Civitas has indeed found that a quarter of 20-to-34 year olds still live with their parents – a million more than two decades ago.

Even in the areas of the country where it’s cheapest to buy property, the rise in the number of adults living with their parents since 1998 is significant – 14% in north-east England and 17% in Yorkshire and the Humber. In London, the figure is a whopping 41%.

Research from Barclays points to a clear contributing factor to this trend. The bank revealed the average deposit for a first-time buyer in the UK in 2021 was approximately £61,000. More than half of those surveyed by the bank admitted they wouldn’t have been able to get a foot on the property ladder without financial help from their families.

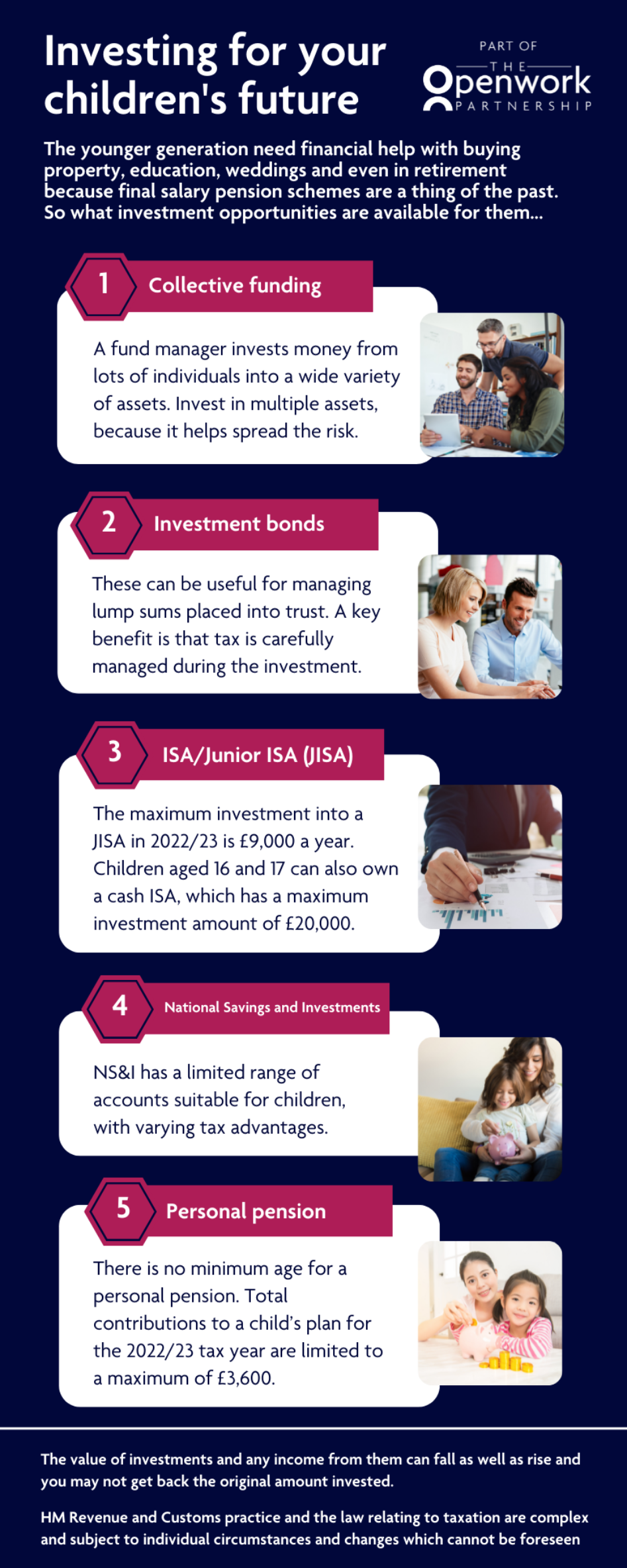

And buying property isn’t the only expense future young adults may need help with: a university education costs approximately £57,000, an average wedding will set you back about £30,000, and even in retirement there’s less security now final salary pension schemes are largely a thing of the past.

So what can Rachel and Samantha do to help their kids?

Happily, there are plenty of options for Rachel and Samantha to consider if they want to start saving for their children’s future.

The two key principles to bear in mind when it comes to investing for your children are:

- The earlier you start saving, the better your potential returns

- Getting professional advice will help ensure you make the right investment decision for your circumstances and avoid potential pitfalls

What kind of investment opportunities are available to Rachel and Samantha?

There are a number of different products that may be suitable for people in Rachel and Samantha’s position. The main ones are:

- Collective funds – a fund manager invests money from lots of individuals into a wide variety of assets. As your money is invested in multiple assets, it helps spread the risk.

- Investment bonds – these can be useful for managing lump sums placed into trust. The underlying investments are usually collective funds but the overall tax treatment is different. A key benefit is that they allow tax to be carefully managed during the investment term and when the investment is redeemed.

- ISA/Junior ISA – Any child under 18, living in the UK, can have a Junior ISA (JISA). The maximum investment into a JISA in 2022/23 is £9,000 a year. Children aged 16 and 17 can also own a cash ISA. The maximum investment for the 2022/23 tax year is £20,000.

- National Savings and Investments (NS&I) – NS&I has a limited range of accounts suitable for children, with varying tax advantages.

- Personal pension - There is no minimum age for a personal pension. Total contributions to a child’s plan for the 2022/23 tax year are limited to a maximum of £3,600.

If you’d like to discuss making investments for your children, we’re happy to help.

The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

Key takeaways:

- The earlier you start saving, the better. This opens up the possibility of long-term investments offering potentially higher returns.

- Get advice from a professional to help ensure you make the right investment choice first time.

- There are a number of investment options that are particularly suitable for those looking to save for their children’s future, including collective funds, investment bonds, ISA/Junior ISAs, NS&I accounts and personal pensions.

- The value of investments and any income from them can fall as well as rise and you may not get back the original amount invested.

- HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

Please note: by clicking this link you will be moving to a new website. We give no endorsement and accept no responsibility for the accuracy or content of any sites linked to from this site.